Pelvic Inflammatory Disease Treatment Market to Reach USD 5.09 Billion by 2034, Driven by Rising STI Cases and Growing Awareness

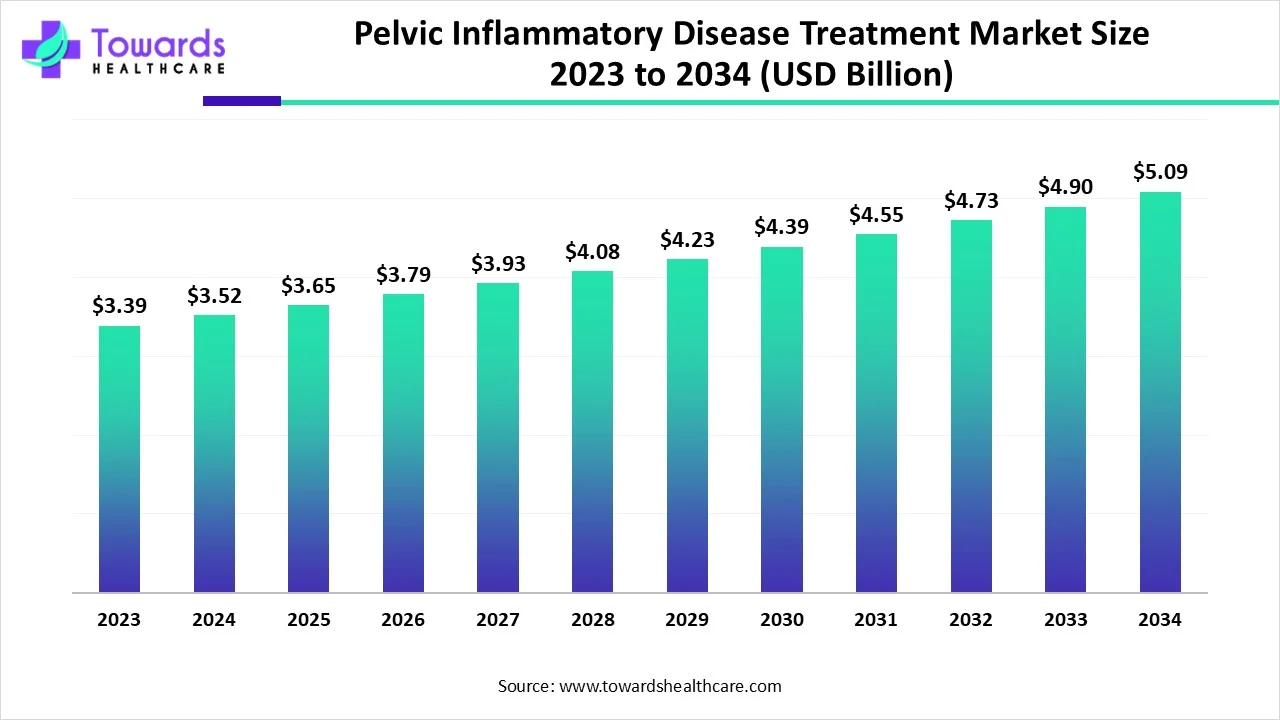

The global pelvic inflammatory disease treatment market size is calculated at USD 3.65 billion in 2025 and is expected to reach around USD 5.09 billion by 2034, growing at a CAGR of 3.75% for the forecasted period.

Ottawa, Nov. 03, 2025 (GLOBE NEWSWIRE) -- The global pelvic inflammatory disease treatment market size was valued at USD 3.52 billion in 2024 and is predicted to hit around USD 5.09 billion by 2034, rising at a 3.75% CAGR, a study published by Towards Healthcare a sister firm of Precedence Research. This market is rising because increasing prevalence of sexually transmitted infections and improved awareness are driving higher diagnosis and demand for effective therapies.

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Key Takeaways:

- North America dominated the global pelvic inflammatory disease treatment market in 2024.

- Asia Pacific is expected to grow at the fastest rate during the forecast period.

- By treatment type, the antibiotic therapy segment dominated the market in 2024.

- By treatment type, the surgery segment is estimated to grow at a notable CAGR during the forecast period.

- By route of administration type, the oral segment dominated the market in 2024.

- By route of administration type, the intravenous segment is expected to grow significantly during the forecast period.

- By patient type, the adult women segment dominated the market in 2024.

- By patient type, adolescent girls segment is anticipated to grow significantly during the forecast period.

- By end user, the hospital segment dominated the global pelvic inflammatory disease treatment market in 2024.

- By end user, the specialty clinics segment is predicted to grow significantly during the forecast period.

Market Overview:

The global market for management of pelvic inflammatory disease (PID) is growing rapidly as there is an increased understanding of women's reproductive health and increased medical focus on the treatment of upper genital tract infection. This market includes therapeutic approaches for infectious and inflammatory conditions of the uterus, fallopian tubes and ovaries resulting from ascending infections with classes of microorganisms, typically bacteria, including Chlamydia trachomatis and Neisseria gonorrhoeae.

Increased access to health care, expanded sexual health education initiatives, and increased screening is resulting in more patients diagnosed and treated earlier. This has resulted in increased uptake of both pharmacological treatments and surgical methods of intervention in addition to improved delivery of care and designated specialized treatment facilities.

The Complete Study is Now Available for Immediate Access | Download the Sample Pages of this Report @ https://www.towardshealthcare.com/download-sample/5518

Major Growth Drivers:

- A primary factor driving the growth of the PID-treatment market is the increasing global incidence of sexually transmitted infections (STIs), which are primary risk factors for developing PID. The higher incidence of chlamydia and gonorrhoea infections in reproductive-age women leads to a larger population of patients requiring treatment.

- A further important lever is increased awareness of possible reproductive health complications (infertility, ectopic pregnancy and chronic pelvic pain), leading patients and providers to undertake more active diagnostic and treatment approaches.

- Meanwhile, advances in availability of healthcare (especially in developing markets) has expanded patient access to clinics, hospitals and diagnostic testing, allowing for earlier intervention and improved management of PID.

- Improvements in antibiotic therapies to include broader-spectrum and combination antibiotics, in addition to minimally invasive surgical techniques, are also driving increased services uptake. Collectively, these factors allow for an improved environment for continued market growth.

Key Drifts:

Emerging Treatment Paradigms:

An important transition in the PID-treatment marketplace is the broadening usage of combination antibiotic regimens and tailored therapeutic approaches as opposed to one-size-fits-all approaches. In many guidelines, coverage is recommended not only for Chlamydia and Gonorrhoea but also for anaerobic bacteria with increased use of metronidazole added to the standard antibiotics.

A second trend is the increased use of out-patient care models, in which patients start to therapy in their homes rather than being admitted to hospital, especially for some of the milder patients. In addition, there is a slow transition to the use of diagnostics that allow for faster identification of pathogens and resistance patterns which facilitates more directed therapy.

Finally, the use of minimally invasive surgery (especially laparoscopic surgery) for the management of turbo-ovarian abscesses or chronic complications is becoming common place and allows for quicker recovery times and lower hospital days as compared to open surgery. All of these trends suggest a movement toward a more individualized, efficient and less invasive approach to the treatment of PID.

Significant Challenge:

Antibiotic Resistance in PID and Gaps in Diagnostics:

A significant barrier for the PID-treatment market is the emergence of resistant organisms and limitations in diagnostics. As standard regimens continue to be faced with non-susceptible bacteria, not only do failure rates increase and the risk of complications increase, but the need for second-line agents or higher level care is also increased.

Furthermore, the lack of an accepted screening test for PID results in many of the cases going undiagnosed (or mismanaged), especially in low-resource settings. The gap in diagnosis means that time is part of the issue, and the risk of sequelae (infertility, chronic pain) goes up with delayed treatment which negates the point of early interventions.

Each of these barriers has contributed to the constraints on PID treatment market growth through reduced optimality of therapy uptake in patient populations needing treatment and creating a greater burden with managing more complex or refractory cases.

Regional Analysis:

In 2024, North America captured the largest proportion of the global pelvic inflammatory disease (PID) treatment market due to a high incidence of sexually transmitted infections and strong reproductive health awareness. There is an advanced healthcare framework in the region paired with improved screening programs and initiatives to facilitate early diagnosis, supported by government bodies and other private organizations. The presence of top pharmaceutical companies and collaborative research efforts are additional stimulating factors for market growth.

The fastest growth is expected to occur in the Asia Pacific pelvic inflammatory disease treatment market during the forecast period. The drivers of growth in the region include increased awareness of sexual and reproductive health, the rise in prevalence of STIs, and improved access to healthcare services. Initiatives to improve female health and increase education on reproductive health have been implemented by government agencies which are increasing rates of diagnosis and treatment in emerging economies such as India, China, and Indonesia. Increased urbanization, improved healthcare infrastructure and investments in female health-related medical programs are factors aiding growth of this market as well.

Become a valued research partner with us - https://www.towardshealthcare.com/schedule-meeting

Segmental Insights

By Treatment Type:

The antibiotic therapy segment had the largest market share in 2024, as it has been accepted as the first-line treatment for PID. The majority of PID cases are attributed to chlamydia or gonorrhoea, therefore antibiotics remain the standard of care. Both oral and intravenous antibiotic treatment regimens are common at outpatient clinics and inpatient settings. Antibiotic therapy has strong preference from both patients and clinicians due to being less invasive than surgery and being able to manage the condition and minimize any future complications early in the treatment timeline. Accordingly, the antibiotic therapy segment can and will continue to grow at a maximum pace as it sees a high volume of cases to treat in addition to established guidelines for treatment.

Surgery is growing, in the form of laparoscopy for abscess drainage or repair of damaged fallopian tubes, in part due to better detection of complications and minimal access surgery. As healthcare systems verticalize in emerging markets, more surgical options will be available to patients who previously had no access to surgery. Surgery can be supported from positive growth in surgery from technology improving time to recovery, morbidity rates and acceptance of the procedure by providers. Surgery is also an option where antibiotics fail or structural sequelae develop driving an additional growth trajectory.

By Route Of Administration Type:

The oral route accounted for the largest market share in 2024 due to the convenience of taking orally, ease of compliance and general patient suitability. Most antibiotic regimens are designed for oral dosing, allowing women to complete therapy in the comfort of their homes and avoid lengthy inpatient admissions.

Likewise, oral therapy fulfils many patient requirements, thus decreasing the burden on healthcare resources, while still allowing for antibiotic therapy to begin rapidly after an initial PID diagnosis is suspected.

Considering that the majority of PID cases are mild to moderate in severity and easily managed in the outpatient arena, these factors become increasingly relevant in defining and subsequently indicating that the oral route will dominate this market segment during this time period.

The intravenous (IV) route, while currently used for a smaller percentage of patients, is on a rapid trajectory for market growth due to the increased number of patients clinically presenting with severe disease, formation of an abscess, or due to antibiotic failure and resistance. The IV route allows for the more rapid onset of therapeutic action, greater bioavailability, and easier management for inpatient hospitals to manage complicated cases.

As hospitals' diagnostic infrastructure is improved and specialized facilities become more common, there will be greater demand for the use of therapy via IV delivery. Once hospitals become utilized to having specialized facilities and engaged in proper upfront assessment and treatment protocols, the IV market segment is likely to see further growth.

Complications with antibiotic failure and subsequent infections will certainly drive additional use of IV routes to accommodate the need for therapeutic use, as resistance rates in PID patients increase.

By Patient Type:

The adult women population accounted for the largest share of the market in 2024, a pattern attributed to the higher rates of PID among women in the reproductive age group. Adult women are more likely to be seen with STIs that will lead to PID, and the potential complications of PID, such as infertility and ectopic pregnancy, are known to drive healthcare resource utilization in this population. Also, adult women tend to engage with the healthcare systems more frequently and are more likely to be screened for STIs, treated and undergo follow-up care, all of which support a higher uptake of therapies. The higher rates of infections, increase in healthcare access and a focus pedagogy in women's health combine to make the adult female population dominate.

The adolescent girl population is projected to witness the largest growth as these young women are becoming more sexually active, are relatively unaware of STIs, and increasingly participate in public health education initiatives that focus on younger patient populations. As the gender-specific health education of adolescent girls expands, we are successfully identifying, screening and treating PID in young women. Additionally, targeted education and public service announcements of sexual health in schools and community programs are likely making adolescents more willing to disclose sexual health issues to clinicians. A higher likelihood of intervention in this population will mitigate potential reproductive issues and concerns, which will drive demand for treatment.

By End User:

In 2024, the highest share by end-user was held by hospitals, since for the majority of PID cases, in particular complicated cases, hospital-based care, hospital-based diagnostic and sometimes inpatient care will be required. Hospitals provide IV therapy, surgical intervention, imaging, and specialists for gynaecology, all key components of the treatment pathway. Many hospital networks have dedicated women’s health departments, protocols for operating on PID cases, as well as programs dedicated to improving women’s access and engagement in care. Due to the preparedness of hospitals to manage acute presentations and complications, hospitals remain the primary channel for treating PID.

Specialty clinics, including women's health and reproductive health clinics, will see considerable growth over the forecast period as they increasingly function as the first-point-of-care for diagnosis and management of PID. These specialty clinics are offering convenient outpatient access, functional expertise, preventive counselling, and other less invasive treatment options that can appeal to patients looking for opportunities for earlier engagement. With rising health awareness and shifting healthcare systems favoring outpatient-led care, specialty clinics will develop a larger share of the administration of this therapy, as this trend will also facilitate market expansion in this end-user category moving forward.

Get the latest insights on life science industry segmentation with our Annual Membership: https://www.towardshealthcare.com/get-an-annual-membership

Recent Developments:

In April 2025, a market study highlighted the increasing uptake of improved antibiotic regimens and minimally invasive surgical techniques in the Pelvic Inflammatory Disease (PID) treatment market, signalling a shift toward more sophisticated patient-care pathways and expanded therapy options.

Key Players in the Pelvic Inflammatory Disease Treatment Market:

| Company | Core Offering(s) | Recent Breakthrough / Major Advance |

| Sanofi | Pharmaceuticals and vaccines with strengths in immunology and rare diseases | Received FDA Breakthrough Therapy designation for tolebrutinib in non-relapsing secondary progressive MS; expanded immunology pipeline with new biologic assets. |

| Bayer | Pharmaceuticals focused on cardiovascular, oncology, and immunology | Achieved full FDA approval for the NTRK inhibitor larotrectinib (Vitrakvi) for NTRK fusion solid tumors; multiple Phase II transitions in pipeline. |

| Johnson & Johnson | Diversified healthcare including pharmaceuticals, medical devices, and consumer health | Investigational therapy nipocalimab granted FDA Breakthrough Therapy Designation for Sjögren’s disease; FDA approval for INLEXZO in bladder cancer treatment. |

| Eli Lilly | Focus on diabetes, obesity, neuroscience, and oncology | KRAS G12C inhibitor olomorasib received FDA Breakthrough Therapy Designation for metastatic NSCLC; continued global success of Mounjaro for diabetes and obesity. |

| Merck & Co. | Oncology, vaccines, cardiometabolic, and respiratory diseases | FDA approval of sotatercept (Winrevair) for pulmonary arterial hypertension; ADC ifinatamab deruxtecan received Breakthrough Therapy Designation for small-cell lung cancer. |

| Novartis | Oncology, ophthalmology, cardiovascular, and immunology | Scemblix (asciminib) received FDA Breakthrough Therapy Designation for newly diagnosed CML; FDA approval of remibrutinib for chronic spontaneous urticaria. |

| AstraZeneca | Oncology, cardiovascular/metabolic, respiratory, and vaccines | Enhertu approved for HR-positive, HER2-low metastatic breast cancer; expanded cell therapy capabilities through acquisition of EsoBiotec. |

| Hoffmann-La Roche | Pharmaceuticals and diagnostics, focusing on oncology, immunology, and neuroscience | Advancing oncology and immunology pipeline, including next-generation cancer immunotherapies and diagnostics integration. |

| AbbVie | Immunology, neuroscience, oncology, and aesthetics | Continued leadership in immunology with Skyrizi and Rinvoq; advancing next-generation therapies in neurodegenerative diseases. |

| Mylan (Viatris) | Generics and biosimilars for global healthcare access | Focus on expanding biosimilar portfolio and accessibility to affordable medicines globally. |

| Abbott Laboratories | Medical devices, diagnostics, diabetes care, and nutrition | Innovation in continuous glucose monitoring (FreeStyle Libre) and advanced cardiac devices. |

| Boehringer Ingelheim | Human pharmaceuticals, animal health, and biopharmaceuticals | Advancing therapies in idiopathic pulmonary fibrosis, oncology, and metabolic diseases. |

| Teva Pharmaceutical | Generics and specialty medicines (CNS and respiratory) | Expanding specialty pipeline in migraine, movement disorders, and respiratory care. |

| Pfizer | Vaccines, oncology, internal medicine, and rare diseases | Entered obesity drug market through acquisition of Metsera; advancing JAK1 inhibitor for atopic dermatitis. |

Segments Covered in the Report

By Treatment Type

- Antibiotic Therapy

- Surgery

- Pain Management

- Hormonal Therapy

By Route of Administration

- Oral

- Intravenous

- Intramuscular

By Patient Type

- Adult Women

- Adolescent Girls

- Pregnant Women

By End User

- Hospitals

- Clinics

- Homecare

By Region

- North America

- U.S.

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa (MEA)

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/checkout/5518

Access our exclusive, data-rich dashboard dedicated to the healthcare market - built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

About Us

Towards Healthcare is a leading global provider of technological solutions, clinical research services, and advanced analytics, with a strong emphasis on life science research. Dedicated to advancing innovation in the life sciences sector, we build strategic partnerships that generate actionable insights and transformative breakthroughs. As a global strategy consulting firm, we empower life science leaders to gain a competitive edge, drive research excellence, and accelerate sustainable growth.

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Europe Region: +44 778 256 0738

North America Region: +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Automotive | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Towards Dental | Towards EV Solutions | Nova One Advisor | Healthcare Webwire | Packaging Webwire | Automotive Webwire | Nutraceuticals Func Foods | Onco Quant | Sustainability Quant | Specialty Chemicals Analytics

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest

![]()

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.